If you thought 2025 AI funding was already absurd, Q1 2026 is going to reset your expectations.

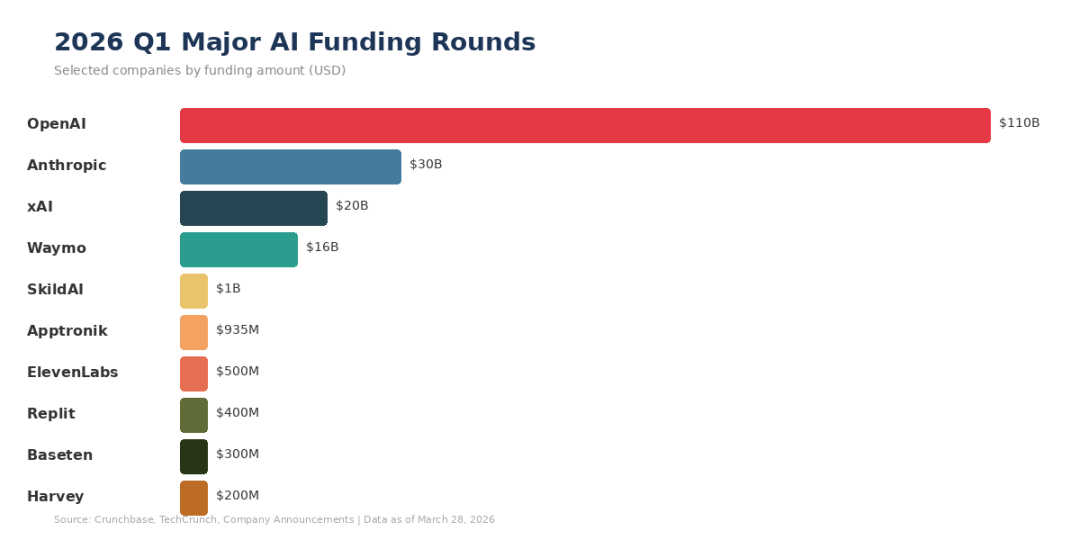

February 2026: $189B raised globally by startups — an all-time single-month record. Even wilder, 83% of that went to three companies — OpenAI ($110B), Anthropic ($30B), Waymo ($16B). AI-adjacent startups consumed 90% of all global venture dollars in the month.

The interesting story isn't the giants' arms race. It's that while the top three were vacuuming up capital, a band of vertical players quietly rocketed up — Replit's valuation tripled to $9B on vibe coding, household robotics company Sunday hit unicorn status straight out of stealth, and legal AI Harvey just hit $11B three days ago.

I dug into Q1 2026's funding stack and there are five clear threads. Each is a different vector of AI moving from concept to real revenue.

Context: a few numbers worth holding in your head

AI startups took 41% of global venture in 2024; by February 2026 it's 90%.

AI startups took 41% of global venture in 2024. That number is 90% in February 2026. That's not just a bubble re-read — the underlying mechanics are interesting. AI companies raise more per round but headcount isn't ballooning, because running the models is structurally expensive. The money is going into compute and infrastructure, not people.

"Round counts are down, but check sizes are up. Fewer bets, but each one is heavier. AI startups raise more not because they have more employees — they raise more because running AI models is expensive." — Peter Walker, Head of Insights at Carta

One useful signal: funds vintage 2023–2024 are seeing some of the best IRR performance of the last decade. The AI wave really is producing returns on paper. The honest caveat: most of that comes from later-round mark-ups, and the question of who actually exits via IPO or acquisition is still wide open.

① Vibe coding — software development's iPhone moment

Replit: the barrier to making software is moving from 'can code' to 'can talk.'

If one word defined 2025's AI app-layer breakout, it's vibe coding — describe what you want in plain language, AI generates the full application. In 2026 the category officially entered the winner-take-most phase.

Replit's arc is more interesting than the growth number alone. It tells a structural story: the barrier to making software is moving from write code to talk. Founder Amjad Masad — Jordanian, started coding at six — spent nine years building "a code editor in the browser" before the vibe-coding wave catapulted him. 2025 revenue: $240M. Target for end of 2026: $1B. 85% of Fortune 500 employees use it.

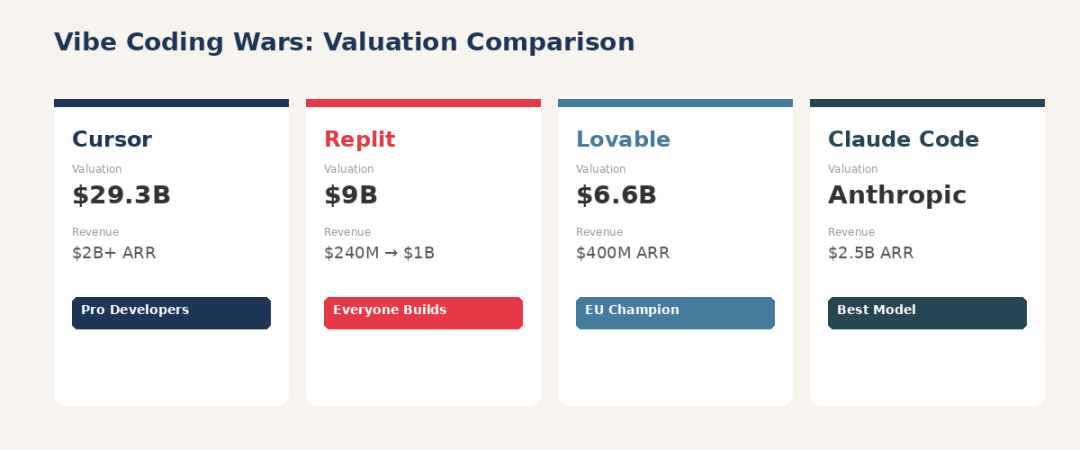

| Company | Valuation | ARR | Positioning | |---|---|---|---| | Cursor (Anysphere) | $29.3B | $2B+ | Pro developer tooling | | Replit | $9B | $240M → $1B target | Software-for-everyone platform | | Lovable | $6.6B | $400M ARR | Europe's strongest vibe-coding play | | Claude Code | Inside Anthropic | $2.5B annualised | Best-in-class coding agent |

A detail I love: two years ago Amjad invited Paul Graham home for a product demo. When Graham instinctively went to look at the generated code, Amjad told him not to bother — "programming is going to be done in English." Graham later called it "mind-bending."

The other side, from Reddit. Don't get fully captured by the funding numbers. The top thread on r/programming is titled Vibe Coding in 2026 is a Complete Scam. One user spent $700/month on Replit, $12K a year. Another quote that captures the mood: "I spent half a day getting the AI to fix what it broke. It told me it was fixed. It wasn't. Then it broke something else." Whether the quality ceiling of vibe coding actually justifies these valuations is the category's biggest open question.

② Household humanoids — from demo to actually in the home

Sunday Robotics' CEO Tony Zhao: 'The point of our Series B is to stop doing demos.'

Robotics formally entered the mega-round era in 2026. The second week of March alone: Mind Robotics ($500M), Rhoda AI ($450M), Sunday ($165M), Oxa ($103M) — over $1.2B combined. Add SkildAI ($1.4B) and Apptronik ($935M) earlier in the year and 2026 robotics funding is on track to clear $20B.

The most interesting one is a company building a robot that does the dishes in your house.

Sunday Robotics. CEO Tony Zhao on their Series B: "The point of this round is to stop doing demos." That line lands. For decades home robotics has been stuck at the lab demo phase. Sunday's differentiation has three pieces:

- Wheels, not legs. Wheeled bases are dramatically more stable and safer than humanoid bipeds.

- "Skill-capture gloves." Mailed to 1,000+ volunteers who recorded real household chores in their own homes. Ten million household "episodes" from 500+ real families trained Memo's base model.

- Cost discipline. Hand-built today around $20K, target retail under $10K.

"Consumers don't want hardware. They don't want software. They want a complete system that solves a problem. Sunday's integrated approach skips the teleoperated-demo era and lands in the world where the robot actually serves the human." — Aaref Hilaly, Bain Capital Ventures

The interesting business primitive here is the data flywheel. Every beta household is a data contributor. Memo learns the layout of your home while it works in it. More households → more data → stronger model → better experience → more households. Same shape as Tesla FSD.

③ Vertical AI — a legal company at $11B

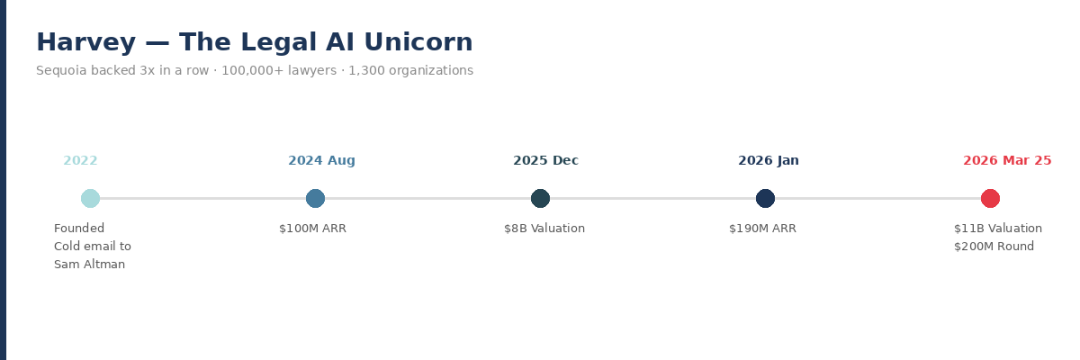

Harvey's round is one of 2026's most significant signals — the vertical app layer can thrive.

While the rest of the field is still arguing whether the app layer has any moat, Harvey answered with the cap table.

Harvey announced their round three days ago (March 25). I think it's one of the most significant signals of 2026 so far, because it makes the proposition concrete: in an era where OpenAI and Anthropic combined exceed a trillion dollars in valuation, the vertical app layer can not only survive, it can thrive.

CEO Winston Weinberg is an ex-lawyer; CTO Gabe Pereyra is ex-DeepMind and ex-Meta research. The company started as a 2022 cold email to Sam Altman. Today: 1,300+ organisations including HSBC and NBCUniversal, 25,000+ custom AI agents built on the platform. Sequoia has led three consecutive rounds — that level of repeated conviction is extremely rare.

"They're writing the textbook for AI-native application companies, the same way Salesforce wrote the textbook for cloud-native application companies." — Pat Grady, Sequoia

The takeaway for founders. Harvey didn't compete with OpenAI on the foundation model. They translated general AI capability into something a regulated, knowledge-dense, workflow-heavy industry can actually use. Law, medicine, financial compliance, tax — all sitting on the same shape of opportunity.

④ AI infrastructure — billion-dollar companies at every layer

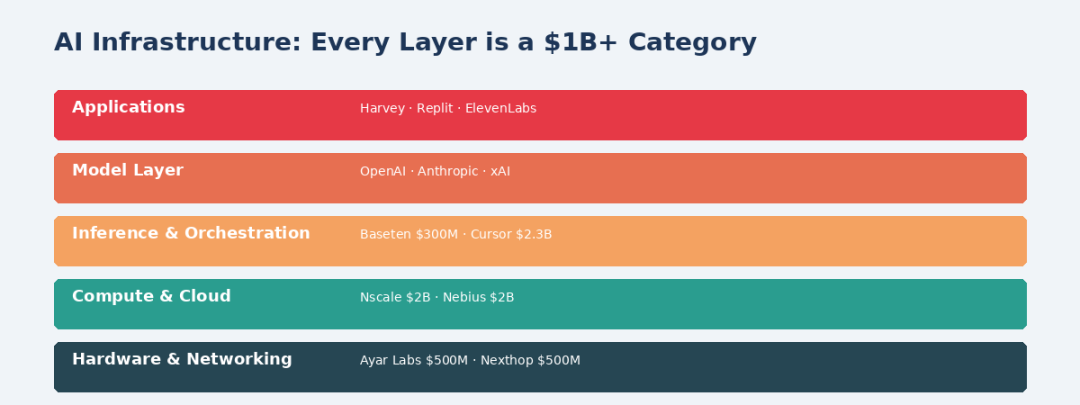

Every layer of the AI data centre is becoming its own billion-dollar category.

A clear 2026 trend: every layer of the AI data centre — chips, networking, storage, orchestration — is becoming an independent billion-dollar investment category.

| Company | Layer | Round | Note | |---|---|---|---| | Nscale | AI data centre | $2B | Europe's largest AI infra | | Nebius | New-style cloud | $2B | Nvidia-backed "neocloud" | | Ayar Labs | Photonic chips | $500M | Light replacing electrons for data transit | | Nexthop AI | AI networking | $500M | Inside-the-data-centre network | | ElevenLabs | Voice AI | $500M | Valuation 3× to $11B | | Baseten | AI inference platform | $300M | Model serving infra |

The "neocloud" rise is the most interesting thread here. AWS / Azure / GCP are massive but generic. AI workloads' demand for GPU clusters is producing a new class of clouds purpose-optimised for training and inference. Nebius took $2B from Nvidia. Nscale is building Europe's largest AI cluster. These aren't competing with the hyperscalers — they're a parallel species.

The other surprise is ElevenLabs. A voice AI company taking $500M Series D, valuation 3× from $3.3B to $11B. Sequoia led; a16z 4× pro-rata'd. Their tech generates near-indistinguishable human voice across 29 languages. When voice AI becomes enterprise infrastructure, the value space opens up dramatically.

⑤ The model-layer giants — the trillion-dollar club

Can't ignore the elephants. February 2026 contained the most dramatic week in private-tech history:

| Company | Round | Post-money | Detail | |---|---|---|---| | OpenAI | $110B | $840B | $50B Amazon, $30B each Nvidia/SoftBank | | Anthropic | $30B | $380B | $14B annualised revenue, Claude Code at $2.5B ARR | | xAI | Merged with SpaceX | ~$1.25T | June 2026 IPO planned |

These numbers exceed most people's intuitions. The real signal isn't the raises — it's the revenue ramps. Anthropic going from zero to $14B annualised is being called the fastest enterprise software revenue ramp in history. Claude Code alone is at $2.5B ARR — a single product, six months out the gate. That's not a bubble cadence. That's a new-era cadence.

What founders should take from this

Looking at these numbers you reach for one of two extremes — "the giants own everything, there's no room" or "there's so much money, just ship anything AI." The reality is between them, with a few sharp judgements:

1. Vertical depth > horizontal breadth. Harvey proved that translating general AI into a specific industry's workflow can build a real moat. Law, medicine, financial compliance, architecture — the depth opportunities here are nowhere near exhausted.

2. Data is the moat. In the AI era, code is generated, models are called over the wire — but high-quality data inside a specific context is hard to replicate. Sunday's household data flywheel. Harvey's legal workflow data. Dash0's production telemetry. Same shape.

3. Speed is everything. Replit tripled in six months. Harvey went $8B → $11B in four months. Sunday hit unicorn straight out of stealth. "Good enough but faster" beats "perfect but slower", decisively, in this market.

4. Be honest about quality. The Reddit complaints about vibe coding are real. So are the reliability problems in home robotics. So are the accuracy risks in legal AI. Funding heat is not product maturity. The thing that decides who survives is whether users actually renew the subscription.

Cold reading. When 90% of monthly venture flows into AI, and 83% of that flows into three companies — is that rational allocation or path dependence? Middle-layer AI startups with no moat (proprietary data, vertical depth, switching costs) are under increasing pressure.

The Q1 2026 funding picture tells one story: bifurcation. Top-tier winner-take-all vs. vertical depth. Speed-first vs. quality moats. Platform ambition vs. specialised value. Whether you're a founder, an investor, or an operator, the point isn't memorising the astronomical numbers. It's seeing the structural forces underneath.

The AI gold rush is still accelerating. But the people who end up holding the gold aren't necessarily the ones who bought the most shovels — they're the ones who knew where to dig.

Data sources: TechCrunch, Crunchbase, CNBC, Bloomberg, company filings and announcements. As of 2026-03-28.